Introduction

No industry dials a phone as often as BFSI, and few pay a steeper price when those calls slip. This guide walks through where AI voice agents earn their place in banking and lending, and the compliance you can't afford to skip.

For Indian banks, NBFCs and insurers, the call centre is the channel where retention, recovery and revenue are decided. A borrower reminded politely before the due date pays on time; a lead qualified within minutes of an enquiry converts far better than one called back two days later. An AI voice agent for BFSI attacks both ends of that problem at once, covering every account in the customer's own language at a fraction of the seat cost, without the variability that makes human calling floors so hard to scale. The catch is that financial calling in India is heavily regulated. Get the operating model and the compliance right, and voice AI becomes one of the highest-leverage automations a lender can run.

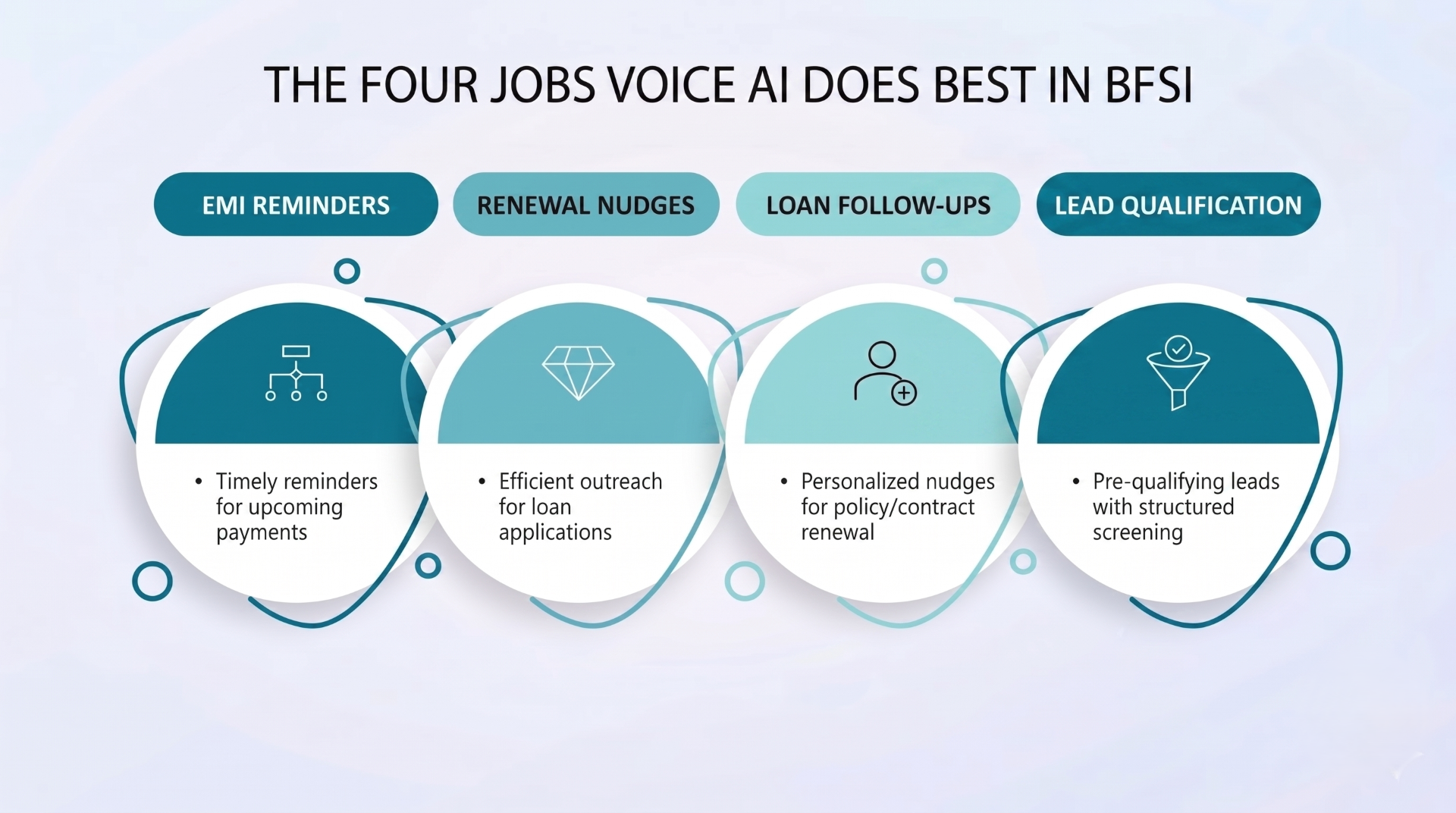

The four jobs voice AI does best in BFSI

Banks, NBFCs, fintechs and insurers churn through more repetitive calls than almost anyone. EMI reminders. Loan follow-ups. Renewal nudges. Lead qualification. The work is high-volume, time-sensitive and tightly scripted, which is why AI voice agents have taken hold here faster than in most of corporate India. A well-built agent covers every account in the customer's own language, without you running a 200-seat calling floor to do it.

The reason these four jobs suit automation so well is that each follows a predictable script with a clear outcome. The agent is not improvising financial advice or negotiating a settlement; it is delivering the same reliable message and capturing a structured response. That makes the work easy to audit and easy to scale. The four highest-value uses for Indian lenders and insurers tend to be:

- EMI and payment reminders before the due date, so on-time payments rise and Day-0 buckets shrink.

- Early-stage loan collections follow-ups that confirm intent, capture a promise-to-pay and flag genuine hardship for a human.

- Lead qualification for personal loans, home loans, credit cards and insurance, filtering enquiries before they reach a salesperson.

- Renewals and policy nudges for insurers and mutual-fund distributors, where a timely call directly protects recurring revenue.

What unites them is volume and consistency. A mid-sized NBFC can have tens of thousands of EMIs falling due in a single week; an insurer may have lakhs of policies up for renewal across a quarter. Human teams ration that work by triaging the largest accounts and leaving the long tail uncalled. An agent simply works the whole list.

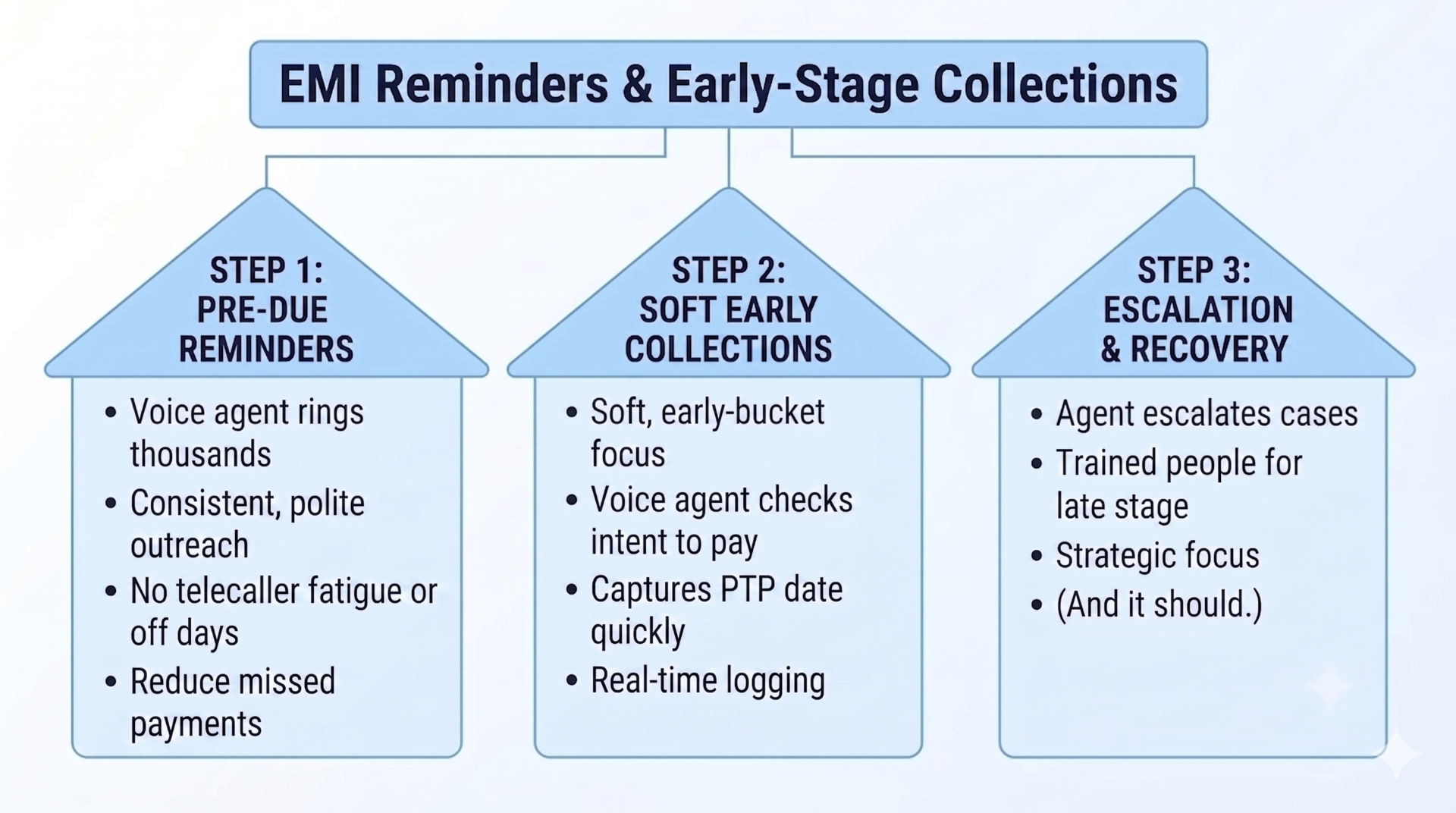

EMI reminders and early-stage collections

A voice agent can ring thousands of borrowers before the due date with the same calm, polite line, "Rahul ji, aapki EMI kal due hai", in Hindi or any regional language. No fatigue by the four-hundredth call, no telecaller having an off day. Get the reminder out a day before, every time, and missed payments drop. In soft, early-bucket collections the agent confirms intent to pay, captures a promise-to-pay date and escalates only the accounts that genuinely need a person, logging every interaction as it goes. The hard, late-stage recovery still belongs with trained people, and it should.

The economics here are straightforward. A large share of EMI delinquency in India is not wilful default but ordinary forgetfulness, a salary that landed late, an auto-debit that bounced for want of balance, a customer who simply lost track of the date. A reminder a day or two ahead catches most of these before they ever become a missed payment, which is why AI voice agent EMI reminders tend to show their value first in the Day-0 and Day-1 buckets. The agent can also offer the borrower an easy next step on the same call: confirm the due amount, share the payment link by SMS, or note a specific date the customer commits to pay.

For loan collections calling, the dividing line matters as much as the technology. RBI's fair-practice expectations and the regulated-entity guidelines on recovery agents are clear that borrowers must be treated with dignity, contacted within reasonable hours, and never harassed or threatened. That maps neatly onto what an agent does well, courteous, scripted, time-bound reminders, and onto what it should never attempt: negotiating a one-time settlement, handling a dispute, or pressing a customer in genuine distress. Those cases must route to a trained human, and a good system makes that handover automatic the moment the conversation moves beyond a simple reminder.

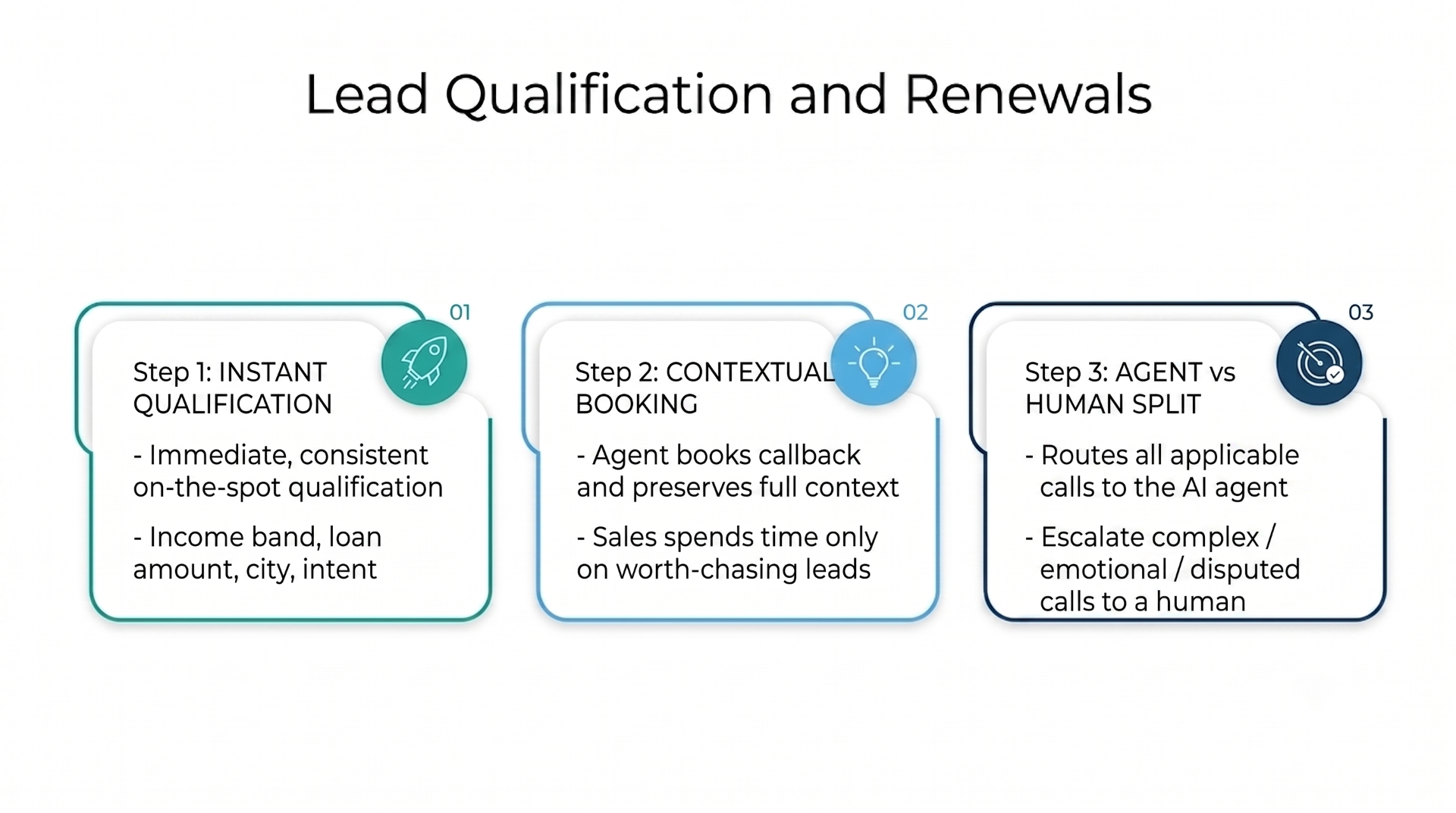

Lead qualification and renewals

An inbound loan or insurance enquiry can be qualified on the spot, income band, loan amount, city, intent, so your sales team spends its hours only on leads worth chasing. The agent books the callback and passes across the full context. Renewals and routine policy questions fit the same mould: consistent, language-matched handling that doesn't hinge on a telecaller remembering what was said last week. The split that works in practice is simple. Let the agent run the routine 70-80% of calls and route anything emotional or disputed to a human, with the context already in hand.

Speed of response is the quiet driver of conversion in lending. When someone fills a form for a personal loan or a top-up, their intent is highest in the first few minutes, and they are usually shopping two or three lenders at once. An agent that calls back instantly to confirm the basics, employment type, monthly income band, requested amount, preferred branch or city, reaches the borrower while they are still leaning in, and arrives at the human salesperson as a warm, pre-qualified lead rather than a cold row in a spreadsheet. The same pattern applies to lead qualification for credit cards, insurance and SIP enquiries.

Renewals are where insurers and distributors quietly leak the most revenue. A motor or health policy that lapses is far harder and costlier to win back than one renewed on a timely nudge. An agent can run the entire renewal reminder cadence, thirty days out, a week out, on the due date, in the policyholder's language, confirm whether they intend to renew, and hand the small share who want to compare plans or change cover to a licensed advisor. For more on the inbound side of this, see our guide on what an AI voice agent is and how the handover to humans works.

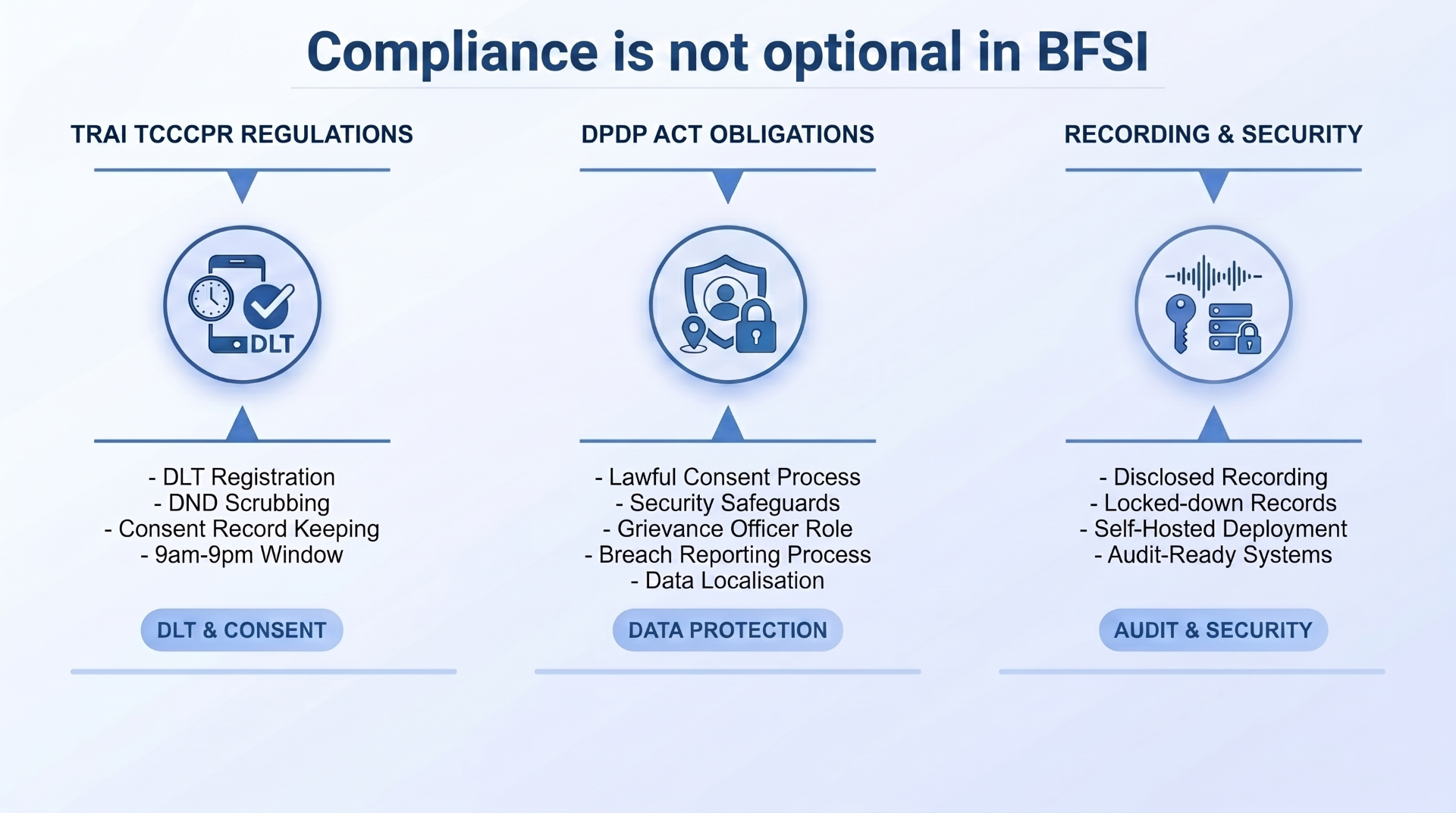

Compliance is not optional in BFSI

This is the part nobody gets to improvise. Financial calling answers to more than one regulator, and the penalties bite. TRAI's TCCCPR demands DLT registration, DND scrubbing, consent records and the 9am-9pm window for promotional calls. The DPDP Act treats borrower data as personal data, so you need lawful consent, security safeguards, a grievance officer, a breach process, and data localisation for sensitive records. Disclose that calls are recorded and keep those recordings locked down. A self-hosted setup, where the data never leaves your own environment, makes audit day a lot less painful. Our guide to TRAI-compliant calling covers the registrations in detail.

It helps to think of compliance for Indian banks, NBFCs and insurers in three layers. The telecom layer is TRAI/TCCCPR: register as a sender, scrub against DND and customer-preference registers, use the correct number series for service versus promotional calls, and keep calls inside the permitted window. The data layer is the DPDP Act: collect borrower data on a lawful basis, store it securely, honour requests for correction or erasure, and have a named grievance officer who can answer a complaint. The conduct layer is sector-specific, RBI's fair-practice code for collections and the IRDAI's norms for how insurance is sold and serviced, which govern tone, timing and what an agent may and may not say.

The practical takeaway is that the technology choice and the compliance choice are the same decision. Where call recordings, consent logs and borrower data physically sit determines how easily you can satisfy an auditor, a regulator or your own risk team. Keeping that data on infrastructure you control, with every call transcribed and timestamped, turns compliance from a scramble into a query.

Knowing whether it's actually working

The teams that get value out of voice AI treat it as an operation with numbers attached. Watch connection and completion rates, promise-to-pay capture, the lift in on-time payments after reminders, qualified-lead conversion, and the share of calls that close without a human. Measure them before and after, split by language and segment, and it becomes obvious where the agent is pulling its weight. The audit trail matters just as much: every call transcribed, timestamped and logged on its own, which is exactly what you reach for when a regulator or your risk team asks what was said and when.

A useful discipline is to run the agent against a control group for the first few weeks, the same borrower segment, half called by the agent and half by your existing process, so the lift in on-time payments or qualified leads is attributable rather than assumed. From there, the gains compound: connection rates improve as you learn the best calling times per region, scripts tighten around the lines that earn the most promises-to-pay, and language routing gets sharper as the agent learns which borrowers prefer Hindi, Tamil or Marathi.

Where to start your rollout

You do not have to automate the entire calling floor on day one, and you should not. The lowest-risk, highest-return place to begin is pre-due EMI reminders for a single product line, say two-wheeler or personal loans, because the script is simple, the outcome is measurable, and there is no negotiation involved. Once that proves out, extend into Day-1 collections follow-ups and inbound lead qualification, where the agent has a warm contact and a clear job. Sensitive late-bucket recovery, dispute resolution and any hardship conversation stay with your trained staff throughout.

Integration is what separates a novelty from an operational tool. The agent needs to read from your LOS, LMS or core system and write back to your CRM so that it knows the account it is calling about, the exact due amount and the borrower's preferred language, and so that every promise-to-pay and disposition lands where your collections and sales teams already work. Treat the pilot as a real operation with owners, targets and a weekly review, and the case for scaling it usually makes itself. You can compare deployment options and seat economics on our pricing page.

Conclusion

BFSI is about as good a fit for voice AI as you'll find, on one condition: the automation has to come with airtight TRAI and DPDP compliance, not as an afterthought.

Five things separate a setup that works from one that gets you in trouble. Native Hindi plus regional voices. CRM and core-system integration so the agent knows the account it's calling about. Compliance built in rather than bolted on. Data ownership, with recordings sitting on infrastructure you control. And a clean handover to humans the moment a call turns into a dispute or a hardship case. 9278.io is built for precisely this. Explore the BFSI use cases or build your first agent.

Ready to put a voice agent on your phones?

Native-audio AI agents in 15+ Indian languages, on Jio/Airtel/BSNL/Vi, live in hours.

Build your first agentFrequently asked questions

How do banks and NBFCs use AI voice agents?

Mainly for EMI and payment reminders, early-stage collections follow-ups, lead qualification for loans and insurance, and renewal nudges, high-volume scriptable calls handled consistently in the customer's language, with humans taking the sensitive cases.

Are AI voice agents allowed for loan collections in India?

Yes, for routine, early-stage reminders and follow-ups, provided you comply with TRAI/TCCCPR rules (DLT registration, DND scrubbing, consent, calling-window limits) and the DPDP Act. Sensitive late-stage recovery should still involve trained human agents.

Can an AI agent send EMI reminders in regional languages?

Yes. India-focused agents deliver reminders in Hindi and regional languages such as Tamil, Telugu, Marathi and Bengali, and can detect the borrower's preferred language, improving comprehension and response rates.

What compliance applies to BFSI voice AI calls?

TRAI's TCCCPR (telemarketer/DLT registration, DND scrubbing, consent, 9am-9pm promotional window, correct number series) and the DPDP Act (lawful consent, security, grievance officer, breach handling, data localisation). Calls must also be disclosed as recorded.

How does AI calling reduce missed payments?

By reliably reminding every borrower before the due date in their own language, with consistent tone and timing. Unlike human teams, an agent never skips accounts or runs out of time, so reminder coverage is complete.

Can the agent integrate with our LMS, CRM or core banking system?

Yes. A practical BFSI deployment reads account details, due amounts and preferred language from your loan management or core system and writes promise-to-pay dates, dispositions and call outcomes back to your CRM, so collections and sales teams see everything in the tools they already use.

When should a call be handed over to a human agent?

Any time the conversation moves beyond a routine reminder, a payment dispute, a hardship or restructuring request, an emotional or distressed borrower, or a settlement negotiation. The agent should escalate automatically with full context, in line with RBI fair-practice expectations for collections.

How quickly can a BFSI voice agent go live?

A focused use case such as pre-due EMI reminders for one product line can be configured, tested against a small batch and taken live in a matter of days, then expanded to collections follow-ups, lead qualification and renewals once the numbers prove out.